The "big, beautiful bill" featuresa new tax break for older Americans who pay taxes on Social Security income. But there's a significant catch.

Why it matters: The break leaves out the poorest seniors, and the very rich ones, too.

How it works: Both the House and Senate bills include an increased tax deduction for tax filers age 64 and older. In the Senate version, the new deduction is $6,000 for individuals and $12,000 for couples.

The deduction starts phasing out for those who earn over $75,000 ($150,000 for couples), and phases out completely at $175,000 for individuals and $250,000 for couples, in the Senate version.

The break expires in 2028 when President Trump leaves office, as do a few other White House priorities in the bills, including no tax on tips, no tax on overtime, and no tax on auto loan interest.

What they're saying: "This amounts to the largest tax break in American history for our nation's seniors," per a report out earlier this week from the White House Council of Economic Advisers.

Yes, but: Most seniors — 64% of them — don't pay taxes on Social Security, according to the White House's own analysis.

Those who can't afford the taxes already don't pay. This break targets most, but not all, of the rest.

Between the lines: Trump promised to eliminate taxes on Social Security income. Lawmakers couldn't pull that off entirely, given the constraints of passing a reconciliation bill and changing Social Security law.

This break comes close. After adding the recipients of the new tax break, 88% of seniors wouldn't pay Social Security tax, per the White House.

"The One Big Beautiful Bill delivers on President Trump's promise of no tax on Social Security," White House spokeswoman Abigail Jackson says in a statement, noting the analysis by the Council of Economic Advisers.

Zoom out: For those upper-middle class folks who pay taxes on retirement benefits, this is a "substantial tax break," says Marc Goldwein, senior policy director for the Committee for a Responsible Federal Budget, a nonpartisan group that advocates for fiscal responsibility.

For the several million senior citizens who live in poverty, and already don't pay taxes on Social Security, this doesn't help.

The bill would also accelerate Social Security and Medicare insolvency by a year, to 2032, per an analysis from the group.

The bottom line: Seniors in the U.S. overall are doing great financially right now, sitting on assets that have soared in value in recent years.

"As a whole seniors in this country are the wealthiest cohort in the history of the known universe," Goldwein says.

If this bill passes, they'll get to keep a little bit more.

Mark Zuckerberg — in an unprecedented, multibillion-dollar talent raid — has dramatically reset the market for blue-chip AI builders, and further complicated the government's ability to stack its own technology bench.

Why it matters: The Meta CEO is trying to lure talent from OpenAI and other tech companies with offers that can top $100 million in total compensation for the first year alone — beyond most star athletes' pay.

Top-tier pay packages being offered by Meta for AI researchers can reach up to $300 million over four years, WIRED reports.

A tech-news feed on X used a baseball card motif to portray an OpenAI researcher being "TRADED" to Meta.

The talent derby has sent compensation soaring across AI, as rivals scramble to keep top talent and entice others not to flirt with Meta and other suitors.

It's partly a continuation of an ongoing recruiting war — OpenAI built its lab with the help of some massive comp packages.

Zuckerberg unveiled his dream team this week as Meta Superintelligence Labs (MSL), after meeting personally with potential recruits at his homes in Palo Alto and Lake Tahoe.

The big picture: America has witnessed staggering valuations for startups. But never before have we seen company-valuation-sized salaries for people, rather than ideas or enterprises.

That's injecting a new layer of drama and next-level economics for the biggest companies — many the size of nation-states — racing to win the AI wars.

Collateral damage: The U.S. government is already struggling to recruit top researchers and scientists. A remotely talented AI specialist can now assume that riches in the tens of millions are attainable. So why sacrifice to serve in government?

China, by contrast, can command top talent to work on government projects. A front-page Wall Street Journal story on Wednesday, "China Is Quickly Eroding America's Lead in the Global AI Race," said AI models from Chinese companies, including DeepSeek and Alibaba, are becoming popular in Asia, Europe, the Middle East and Africa.

Zoom in: Zuckerberg's biggest single bet was investing $14 billion in Scale AI, and bringing co-founder Alex Wang to Meta as chief AI officer. Former GitHub CEO Nat Friedman will lead Meta's work on AI products and applied research.

Eleven other new AI star hires were listed in Zuckerberg's internal memo announcing Meta Superintelligence Labs.

Altman hit back at Zuckerberg's spree this week, telling OpenAI researchers in a Slack message that Meta "has gotten a few great people for sure, but on the whole, it is hard to overstate how much they didn't get their top people and had to go quite far down their list," WIRED reports.

"I am proud of how mission-oriented our industry is as a whole; of course there will always be some mercenaries," Altman added. "Missionaries will beat mercenaries."

Between the lines: Tech investors tell us that until very recently, the revenue outlook for AI models was unclear, and there was a debate about the return on capital spending. Now it's apparent that leading AI companies will do hundreds of billions in revenue per year.

OpenAI is enjoying rampaging growth: The company said last month that it has $10 billion in annual recurring revenue, just 2½ years after the launch of ChatGPT — up from $5.5 billion last year. OpenAI has projected for investors that, fueled by AI agents and other new products, sales could total as much as $125 billion in 2029 and $174 billion in 2030, according to documents seen by The Information.

Anthropic — a rival AI company led by Dario Amodei, an OpenAI alumnus — has hit a pace of $4 billion in revenue annually, up almost four times from January, The Information reported this week.

At those rates of growth, you can see what Zuckerberg is seeing — and why he's suddenly pouring massive spending into making sure Meta remains a dominant AI player.

The backstory: Zuckerberg is repeating a winning playbook. By 2012, he realized Facebook was behind on the mobile web. He famously redirected the entire company toward catching up.

Facebook bought Instagram for $1 billion and later WhatsApp for $16 billion — racing ahead in areas where others had innovated. But this time he's betting on individuals, rather than successful enterprises.

Reality check: Meta has spent a fortune on Llama, its large-language model (LLM), in an effort to develop a frontier model that can compete with OpenAI's ChatGPT, Anthropic's Claude and Google's Gemini. In a splashy story about "The List" of AI geniuses Zuckerberg is courting, the Wall Street Journal said Meta's "laggard history in generative AI has made some recruits hesitant."

Bubbles can burst. AI salaries and data-center costs won't be sustainable without the ultimate payoff being unimaginably huge. And the more these companies spend, the bigger that payoff needs to be. As uncovered by a survey Axios reported last month, many small businesses using AI aren't even paying for it.

The other side: Altman, noting that OpenAI has built "a culture that is good at repeatable innovation," said last month on a podcast hosted by Jack Altman, his younger brother, that Meta was making "giant offers to a lot of people on our team — like $100 million signing bonuses" and more than that in annual compensation.

"We're set up such that if we succeed ... then everybody will do great financially," Sam Altman said. "[I]t's incentive-aligned with mission-first, and then economic rewards and everything else flowing from that."

The bottom line: The bidding war is the most public manifestation of the secret race among AI giants — all betting that the technology will bring trillions of dollars in productivity gains. For them, the timeline is the biggest question.

Axios' Scott Rosenberg, Ben Berkowitz and Zachary Basu contributed reporting.

Go deeper ... "Behind the Curtain: An AI Marshall Plan."

The demise of a controversial proposal in Republicans' budget bill that blocked state-level regulation of artificial intelligence is fueling fresh pressure for federal action, advocates told Axios Wednesday.

Why it matters: Congress' reluctance to set national AI rules for privacy, safety and intellectual property rights has left states to forge ahead with their own rules.

Driving the news: Some senators fought until the last minute to keep an industry-backed 10-year ban on state-level regulation in the budget bill.

Senator Ted Cruz (R-Texas) and some of his allies in the administration fought until the last minute to keep an industry-backed 10-year ban on state-level regulation in the budget bill. They failed — for now.

"We hope that this unequivocal rebuke to the idea of saying that states can't regulate AI is a lot of political motivation for the folks who do want to regulate AI on Capitol Hill," said Eric Kashdan, Campaign Legal Center's senior legal counsel for federal advocacy.

Catch up quick: The Senate early Tuesday voted nearly unanimously to remove the proposed moratorium on state-level AI regulations from the budget bill.

It would have prevented states that want certain government grants from enforcing legislation on AI regulation.

"The reconciliation package was the best possibility for something this bad to get through," said Alix Fraser, the vice president of advocacy for Issue One.

The House passed a version of the budget bill that included the state AI moratorium, but the Senate's version, which dropped it, now faces resistance from some House Republicans.

Friction point: PresidentTrump's aides and advisers were split on the moratorium.

While many have favored a light hand with AI to bolster U.S. efforts to keep ahead of China, others are concerned that the moratorium rules would also make it harder for states to regulate social media, particularly around protecting kids.

Former Trump adviser Steve Bannon helped fuel opposition, the Wall Street Journal reported, and many in the MAGA movement still believe Big Tech has stifled conservative voices.

"Bannon has never been a fan of this sort of techno utopia that a lot of Silicon Valley-ites desire, and the idea of a moratorium was antithetical to that approach," Fraser said.

Zoom out: More than 20 Democratic- and Republican-led states have passed AI regulation legislation.

An April Pew study found the public is worried the government won't go far enough in regulating AI.

Most Americans support a national AI standard and think a patchwork of state laws will make it harder for the U.S. to compete with China, according to a June Morning Consult and TechNet poll.

"There's a huge public demand for AI to be regulated, a bipartisan demand for AI to be regulated," Kashdan said. "And not only will they give up on trying to start states from stepping up but they'll recognize that this means they really need to get their act together and pass federal AI regulations."

Yes, but: Congress has always had a hard time passing laws regulating tech, and the mood in Washington right now is favoring innovation over regulation

Efforts to regulate AI at the federal level are unlikely to go as far as consumer protection measures in the states.

What's next: The battle over a moratorium is not over, said Chris MacKenzie, vice president of communications for Americans for Responsible Innovation.

Advocates expect standalone legislation to try to preempt state AI laws.

Data: Dallas Fed; Note: Firms limited to those located or headquartered in the Federal Reserve's eleventh district; Chart: Axios Visuals

President Trump wants to "drill baby drill." But many producers in the heart of the oil patch have other plans — and some say Trump's trade policies are discouraging drilling.

Why it matters: Many things affect gasoline prices. But producers' caution about growing output could limit how much prices at the pump might fall by helping avoid a large market glut of oil.

Driving the news: The Federal Reserve Bank of Dallas on Wednesday released its latest quarterly survey of execs in its region that includes the prolific Permian Basin.

These anonymous surveys are hot commodities for anyone seeking the industry pulse.

Threat level: "The Liberation Day chaos and tariff antics have harmed the domestic energy industry," one executive told the Fed.

"Drill, baby, drill will not happen with this level of volatility. Companies will continue to lay down rigs and frack spreads," said the exec, one of several who criticized the tariffs.

State of play: The poll of exploration and production (E&P) firms and drilling contractors showed overall activity contracting slightly in Q2, and production dipping slightly.

Looking ahead, the poll's average of price forecasts is $68 per barrel over the next year for WTI, the benchmark U.S. grade, roughly where it's at now.

"Almost half of executives surveyed expect to drill fewer wells in 2025 than they planned at the start of the year," it states.

Large producers (10,000+ barrels per day) were more likely to see drilling "significantly" fall.

What we're watching: Prices and input costs.

If they drop to $60 per barrel and stay there, 61% expect their production to fall slightly over the next 12 months, while 9% see a big drop (see above).

Twenty-seven percent of execs say the recent steel tariff hike will mean slightly fewer wells drilled, and 5% expect significantly fewer.

Flashback: The Q1 survey showed that on average, firms say they need oil at $65 to profitably drill new wells.

The latest outlook from the Energy Department's independent stats arm projects a slight drop in the second half of this year, and a slight annual decline in 2026.

Yes, but: A White House spokeswoman said Trump is making drilling easier by rolling back "stifling" Biden-era regulations.

"The One, Big, Beautiful Bill's tax cuts and full equipment expensing will further turbocharge growth and investment by oil and gas companies — another reason Republicans need to get this bill across the finish line and onto the President's desk," Taylor Rogers said in a statement.

The big picture: U.S. output is already at record levels and the country is by far the world's largest producer.

Trump's "dominance" agenda includes more drilling access in offshore areas and Alaska. But those are very long-term projects.

Today's economic picture, combined with shale producers' focus on capital discipline and shareholder payouts, is working against near-term growth.

What we're watching: The global market, which sways domestic drilling decisions.

OPEC+ will meet July 6 to decide on its next tranche of output increases.

Press freedom advocates are sounding the alarm following Paramount's $16 million settlement with President Trump, arguing the deal sets a dangerous new precedent, particularly for smaller outlets with fewer legal resources.

Why it matters: A steady decline in media trust, coupled with enormous financial challenges, has made the press more vulnerable to political pressure campaigns than ever before.

Between the lines: The deal has drawn outrage from critics who believe Paramount could have won what they believe is a frivolous lawsuit.

Democratic Sens. Ron Wyden and Elizabeth Warren both called the settlement "bribery."

The Knight Institute said Paramount's legal exposure was "negligible," and argued it should've fought the case in court.

PEN America, another press freedom group, said Paramount "caved to presidential pressure" and "chose appeasement to bolster its finances."

Reality check: The Wall Street Journal editorial board on Wednesday noted that this moment feels like a turning point for press freedom.

"President Trump has taunted the media for years, and some of his jibes are deserved given the groupthink in most newsrooms. What's happening now, though, is different: The President is using government to intimidate news outlets that publish stories he doesn't like. It's a low move in a free country with a free press," it wrote.

Zoom out: The settlement comes as the administration ramps up its efforts to target the press.

Most recently, President Trump and Department of Homeland Security Secretary Kristi Noem have endorsed the idea of prosecuting CNN for its critical coverage of U.S. strikes in Iran and its immigration reporting.

President Trump also suggested he could demand journalists reveal their sources in light of the Iran intel leak. In April, the Justice Department repealed protections for journalist-source confidentiality

The White House has already banned the AP over its editorial standards. It's also pushing Congress to gut funding for public media. The FCC has launched investigations into Comcast/NBCU and Disney/ABC for their DEI policies.

The big picture: The Paramount settlement is the latest in a slew of recent examples that show just how desperate media companies are to survive political and economic pressure.

Disney, Warner Bros. Discovery, Paramount, Gannett and other major media companies have all rolled back diversity, equity and inclusion policies to mirror the administration's new mandate on DEI.

The vast majority of America's largest newspapers by circulation are no longer doing presidential endorsements.

PBS member WNET cut 90 seconds from a documentary last month, in which the film's subject, author and cartoonist Art Spiegelman criticized Trump, per The Atlantic.

ABC News dropped longtime correspondent Terry Moran after he criticized President Trump and top aide Stephen Miller in a since-deleted tweet, drawing swift criticism.

What to watch: Those concessions are happening amid a historic drop in trust of mainstream media, making it harder for newsrooms to rally public support.

Only 31% of Americans say they have a great deal or a fair amount of trust in the mass media, down from 50% 20 years ago and 40% a decade ago, according to a Gallup survey.

House Speaker Mike Johnson (R-La.) said early Thursday morning he believes he has the votes to get President Trump's "big, beautiful bill" across the finish line in the coming hours, "right when everyone is waking up to have their coffee."

Why it matters: Johnson is racing against the clock to meet Republicans' self-imposed deadline to pass the marquee tax and spending bill, which they hope will get to the president's desk by July 4.

That deadline is at threat of slipping as right-wing hardliners and moderates dig in against the bill over aspects they find unsavory.

Republicans on Thursday broke the record for the longest House vote as they held open a procedural vote for an astonishing seven hours and 24 minutes as they tried to cajole GOP holdouts.

Johnson continued to huddle with holdouts off the House floor past midnight, and Trump has been working the phones in coordination with Johnson, the speaker said on Fox News.

State of play: Shortly after concluding their record-breaking vote, Republicans moved to advance the bill to a final vote on the House floor.

But that key vote was being stymied by GOP defectors as of early Thursday morning, with nearly half a dozen Republicans voting with Democrats against advancing the bill — enough to kill it.

Another group of around eight Republicans — mostly right-wing hardliners upset at how much the Senate version of the bill increases the deficit — hadn't voted yet as of Thursday morning.

A group of key holdouts left the House floor just after 1:00am and headed back to their offices, including Rep. Tim Burchett (R-Tenn.), who told reporters "don't take a nap" yet. Burchett has still not voted on the rule.

What they're saying: "There's no cracking of skulls ... this is part of the process. We're tying up loose ends," Johnson told Fox News host Sean Hannity in an appearance late Wednesday night.

The speaker said he "might keep [the vote] open a little while" because "among those 'no' votes I've got a couple of folks that are actually off-site right now, had to attend family affairs or events this evening, and so some of them are on the way back."

That includes Rep. Brian Fitzpatrick (R-Pa.), the sole centrist "no" vote on the procedural motion, who rushed out of the House chamber shortly after voting.

Rep. Thomas Massie (R-Ky.) who doesn't typically vote down the rule, switched his vote from yea to nay last minute, and has stayed firm in his opposition.

Between the lines: Rep. Victoria Spartz (R-Ind.) posted on X that she intends to support final passage of the bill, but voted against the procedural measure because of Johnson's "broken commitments."

It's not typical for a member of the majority party to vote down the rule, and even more abnormal to vote down the rule but support final passage.

Some members, like Spartz, are notorious for saying they're a no but voting yes.

Rep. Ralph Norman (R-S.C.) vowed to vote no on Wednesday, but then voted yes on the rule.

Kilmar Ábrego García alleged in an amended complaint Wednesday that he "was subjected to severe mistreatment" while detained in the El Salvador mega-prison CECOT after being mistakenly deported to the country.

The big picture: The U.S. resident who spent nearly three months in CECOT is now detained in Tennessee after being returned to the U.S. and is awaiting trial on human smuggling charges, to which he has pleaded not guilty.

A federal judge had last week ordered his release from prison, but another judge ruled on Monday that Ábrego García should remain in jail for now over concerns from his legal team that he could be deported if freed while awaiting trial.

Driving the news: Lawyers for Ábrego García alleged in a Wednesday filing that the father, who is originally from El Salvador, "was subjected to severe mistreatment upon arrival at CECOT, including but not limited to severe beatings, severe sleep deprivation, inadequate nutrition, and psychological torture."

Zoom in: Among the allegations outlined in the filing to the District Court of Maryland are that Ábrego García and 20 other Salvadorans were "forced to kneel" in a cell from 9pm to 6am "with guards striking anyone who fell from exhaustion."

It adds, "During this time, Plaintiff Abrego Garcia was denied bathroom access and soiled himself. The detainees were confined to metal bunks with no mattresses in an overcrowded cell with no windows, bright lights that remained on 24 hours a day, and minimal access to sanitation."

Ábrego García allegedly suffered a significant deterioration in his physical condition during his first two weeks at CECOT and his weight dropped from about 215 pounds to 184lb, according to the filing.

The lawyers allege that Ábrego García and four others were transferred in April "to a different module in CECOT, where they were photographed with mattresses and better food — photos that appeared to be staged to document improved conditions."

What they're saying: The Trump administration has accused Ábrego García of being a criminal and a member of the MS-13 gang, which his attorneys have denied.

Department of Homeland Security Assistant Secretary Tricia McLaughlin doubled down on this assertion in a Wednesday evening statement.

McLaughlin also called him an "alleged human trafficker, and a domestic abuser" — in reference to allegations made by his wife, who said she sought a "civil protective order" out of caution after "surviving domestic violence" in a previous relationship.

"The media's sympathetic narrative about this criminal illegal gang member has completely fallen apart, yet they continue to peddle his sob story," McLaughlin said. "We hear far too much about gang members and criminals' false sob stories and not enough about their victims."

Representatives for the Justice Department and Customs Enforcement did not immediately respond to Axios' request for comment on Wednesday evening.

The "big, beautiful bill" is a dense, 940-page bill put together last minute.

The big picture: Experts agree the breakneck speed of deliberation over what's in the bill leaves plenty of minutia and changes to sift through.

"This is not normal," said Harris Eppsteiner, associate director of economic analysis at the Yale Budget Lab. "This pace of legislating is not what you would expect to see of a careful, well-thought out set of policies that are designed to grow the economy, help people save and help people invest."

"I never seen something like this, to be honest," said Ignacio González, co-director of the Institute for Macroeconomic and Policy Analysis at American University.

Here's what economic and policy experts said people should watch out for with the "big, beautiful bill" as it heads to the House.

How BBB impacts gambling

Context: The new bill puts the amount gamblers can deduct from their winnings equal to 90% of their losses for a tax year. This rule would be permanent and start in 2026, said Garrett Watson, director of policy analysis at the Tax Foundation.

This means that a hypothetical gambler who won $100,000 but lost $100,000 would have to pay taxes on $10,000 of income.

What they're saying: "Even if you break even, you'll still have a tax liability under this proposal," Watson said. "There could be scenarios where folks have a tax liability that matches or exceeds the amount that they earn."

Pro poker player Phil Galfond said on X this amendment "would end professional gambling in the US and hurt casual gamblers."

Charitable giving

What to know: Under current law, taxpayers who itemize their deductions can receive deductions from charitable donations, Watson said. The new bill allows those who take the standard deduction to deduct up to $1,000 (single) or $2,000 (joint).

Most Americans don't itemize their tax reductions, Watson said, but this gives people the chance to benefit.

"Many people give at least some things during a year that could qualify," Watson said. "They can take that and then take that deduction from their taxes and it reduces their taxable income, reduces their tax liability at the end of the day. "

Car loan interest and the BBB

The current version includes an auto loan interest deductible, which includes provisions that expire in 2028. Some taxpayers could deduct up to $10,000 of annual interest on new auto loans, according to Watson.

Loans for used cars would not qualify under the Senate version, Watson said, and the benefit only applies to new autos assembled in the United States.

Reality check: Jonathan Smoke, chief economist at market research firm Cox Automotive, downplayed the benefits of it, saying a new loan would see roughly $500 in savings.

"The interest payment on an average loan being closer to $3000 in interest in a calendar year and declining over time," he said in an earnings call in June. "So when you factor in what that really means to your taxes of taking the credit, it essentially is not even what a single monthly payment turns out to be."

(Disclosure: Cox Automotive is owned by Cox Enterprises, which also owns Axios.)

Rising electricity bills due to BBB

Context: The bill phases out tax credits for solar and wind projects — meaning that development will slow and consumers will face higher prices.

This is happening at a time when electricity demand has risen given its needed for artificial intelligence and data centers.

"They're going to face higher electricity" rates, said Natasha Sarin, president and co-founder of the Budget Lab at Yale.

Energy economists and others have been predicting prices will rise. Republicans argue that over time, as more generation is added, prices will level out and eventually drop.

Consumer protections targeted in BBB

Funding for the Consumer Financial Protection Bureau, a small operation that fights big businesses on behalf of American consumers, has been slashed by about half in the new bill.

The CFPB has already been limping along after layoffs and legal troubles.

The severed funding could lead to hundreds of job cuts and severely disarm a group that has returned billions to American consumers for more than a decade, according to AP.

"Consumers will be more likely to fall victim to shady financial industry practices, hidden fees, and other scams because of this devastating budget cut," said Chuck Bell, advocacy program director at Consumer Reports, in a statement.

President Trump's asylum ban at the U.S.-Mexico border enacted in an emergency immigration proclamation on his first day in office is "unlawful," a federal judge ruled Wednesday.

Why it matters: Although U.S. District Judge Randolph Moss postponed his order from taking effect for 14 days to allow for appeal, the processing of asylum claims at the border would resume immediately if the ruling is not overturned.

Trump administration officials have already said they'll appeal Moss' ruling that found the president exceeded his authority in a Jan. 20 proclamation that denied asylum protections at the border.

The case seems likely headed for the Supreme Court, which last week in a majority ruling imposed new limits on lower courts' abilities to freeze federal policies.

Driving the news: The proclamation that's titled "Guaranteeing the States Protection Against Invasion" states the Immigration and Nationality Act "provides the President with certain emergency tools" that have enabled Trump's action.

Immigration groups including the American Civil Liberties Union and multiple people seeking asylum filed a class action lawsuit in February challenging the legality of the proclamation, calling the "invasion" declaration unlawful and false.

"[N]othing in the INA or the Constitution grants the President or his delegees the sweeping authority asserted in the Proclamation and implementing guidance," Moss wrote. "An appeal to necessity cannot fill that void."

The Constitution doesn't give a president authority to "adopt an alternative immigration system, which supplants the statutes that Congress has enacted and the regulations that the responsible agencies have promulgated," according to the Obama-appointed D.C. judge.

Between the lines: The attempted asylum changes are among many immigration enforcement reforms the Trump administration is trying to make via executive order or rule changes without going to Congress.

The Trump administration issued a new rule in January that dramatically expands expedited removal to immigrants who cannot prove they have been continuously living in the U.S. for over two years.

The Trump administration also is trying to make immigrants previously granted humanitarian parole eligible for expedited removal, and that's also facing a legal challenge.

What they're saying: ACLU of Texas legal director Adriana Piñon said in a statement Moss' rejection of the Trump administration's "efforts to upend our asylum system" was "a key ruling" for the U.S.

"This attempt to completely shut down the border is an attack on the fundamental and longstanding right to seek safety in the U.S. from violence and persecution."

Keren Zwick, director of litigation at the National Immigrant Justice Center, which also brought the suit, said in a statement that no president "has the authority to unilaterally block people who come to our border seeking safety."

The other side: "A local district court judge has no authority to stop President Trump and the United States from securing our border from the flood of aliens trying to enter illegally," said Abigail Jackson, a spokesperson for the White House.

"This is an attack on our Constitution, the laws Congress enacted, and our national sovereignty," she said of the ruling. "We expect to be vindicated on appeal."

White House deputy chief of staff Stephen Miller on X claimed the order was trying to "circumvent" last week's Supreme Court ruling and that it declared undocumented immigrants as "a protected global 'class' entitled to admission into the United States."

House Republicans broke the record Wednesday for the lower chamber's longest vote in history after more than seven hours of grueling negotiations over President Trump's "big, beautiful bill."

Why it matters: The extended vote time reflects the severe reluctance among some on the House GOP's right flank to support the marquee tax and spending package.

The previous record was in 2021, when the House took seven hours and six minutes on a procedural vote related to then-President Biden's Build Back Better legislation.

House Republicans overtook that record at 9:15pm ET on Wednesday, then went another 15 minutes before finally closing the vote.

Assistant House Minority Leader Joe Neguse (D-Colo.) needled Republicans on the vote time by suggesting they were violating House rules by holding the vote open for so long.

State of play: The lengthy vote came about as a result of negotiations between House Speaker Mike Johnson (R-La.) and members of the right-wing Freedom Caucus.

The hardliners are upset that the Senate bill adds more to the deficit than the House-passed version while also excluding several key provisions they secured to cut green energy tax credits and Medicaid.

Some moderates have also had concerns about the bill, saying it cuts too much into Medicaid and other key programs.

Secretary of Homeland Security Kristi Noem said during a public meeting on Wednesday that she is trusting advisers to provide counsel on how to fire people who "don't like us."

Why it matters: Noem's comment sends a chilling message to the DHS, which has gone through a mass exodus and public backlash over its immigration policies.

Zoom in: During the first Homeland Security Advisory Council meeting held at the DHS headquarter, Noem gave opening remarks by saying there is a lot of people in the department "that don't support what we are doing."

"What we have to be aware of is that we're working with the department that for the last four years hasn't been required to do much," Noem said.

She then blamed former Secretary Alejandro Mayorkas for telling DHS workers "not to do a lot."

Zoom out: The Trump administration has been increasingly vocal about drastically restructuring the DHS.

Noem has privately supported the idea of shrinking FEMA's role in disaster planning, per CNN. She later walked back the claim.

Officials staffing the U.S. legal immigration system have been asked to volunteer to help deportation operations spearheaded by ICE, according to CBS.

Context: The advisory council consists of 22 members appointed by President Trump and Secretary Noem. The council provides the secretary of Homeland Security with real-time, real-world and independent advice on homeland security operations.

Notable members include former New York City Mayor Rudy Giuliani, billionaire Marc Andreessen, and Fox News host Mark Levin.

The White House on Tuesday published a list of staff salaries, revealing how much each West Wing employee makes.

Why it matters: The annual report to Congress gives a peek into the more than 400 staffers who surround President Trump, from his closest advisers to more junior aides.

The intrigue: With a salary of $225,700, adviser Jacalynne B. Klopp is the top-paid person in the White House.

Second is associate counsel Edgar Mkrtchian who makes $203,645.

What should have been a five-minute procedural vote on President Trump's "big, beautiful bill" has stretched for more than 90 minutes with no clear end in sight due to firm opposition from some corners of the GOP.

Why it matters: House Republican leaders are working furiously to pass the sweeping reconciliation bill before their stated July 4 deadline — but persistent delays threaten to put that goal out of reach.

A group of GOP deficit hawks have been meeting off the House floor since returning from their meeting at the White House.

State of play: An hour into the vote, Republicans were told to head back to their offices and sit tight while more meetings occur, per a source familiar with the matter.

Lawmakers in both parties were told they will have at least an hour before they are needed back on the floor, aides and members told Axios.

In addition to intra-party defections, Republicans have also been wracked by weather-related tardiness and absences from their members.

A group backed by White House Deputy Chief of Staff Stephen Miller has filed a federal complaint against the Los Angeles Dodgers over the team's diversity, equity, and inclusion (DEI) practices.

Why it matters: The Dodgers are one of the most popular MLB teams among Asian, Black and Mexican American fans and recently committed $1 million to help immigrants affected by President Trump's immigration raids in Southern California last month.

The big picture: The complaint is part of a larger strategy by MAGA conservative-led groups to attack private companies that are keeping programs aimed at helping or recruiting people of color.

Zoom in: America First Legal (AFL) announced this week it has filed a federal civil rights complaint with the U.S. Equal Employment Opportunity Commission (EEOC) against the Dodgers and the investment firm Guggenheim Partners.

The group says the reigning World Series champions are "engaging in unlawful discrimination under the guise of 'diversity, equity, and inclusion' (DEI), in violation of Title VII of the Civil Rights Act of 1964."

The complaint alleges that the Dodgers "appear to be engaging in similar unlawful DEI practices by allowing race, color, and sex to motivate employment decisions."

AFL specifically attacks Dodgers' programs that seek to help Asian Americans, Black Americans and Latinos, which the group claims are unlawful.

The Dodgers and controlling owner Mark Walter's Guggenheim Partners did not immediately respond to Axios for comment.

The team participated on Sunday in a "Salute to the Negro Leagues" game against the Kansas City Royals where Dodgers player wore Brooklyn Dodgers caps.

The intrigue: AFL in its announcement cited the Dodgers saying U.S. Immigration and Customs Enforcement agents were denied access to parking lots outside Dodger Stadium last month.

MAGA conservatives responded angrily on social media to the Dodgers, and the Department of Homeland Security denied that it had asked for access.

Between the lines: The complaint comes as Trump's Justice Department is using a broad reinterpretation of Civil Rights-era laws to focus on "anti-white racism" rather than discrimination against people of color.

In March, MLB removed the word "diversity" from its MLB Careers home page in reaction to Trump's executive order ending "equal opportunity" for people of color and women in recruiting.

The change appears to affect MLB's Diversity Pipeline Program, which Baseball Commissioner Rob Manfred launched in 2016.

What they're saying: "Stephen Miller's group is dressing up vengeance as legal action," Jared Rivera, chief of staff of the advocacy group PICO California, said after the complaint was filed.

Retaliating against the Dodgers for their compassion shows Miller is threatened when the team and its fans stand up for what is moral and right."

PICO California was one of the groups urging the Dodgers to speak out more about the immigration raids.

Context: The Dodgers had come under criticism earlier this month for failing to speak out against ICE raids in LA and for unsuccessfully pressuring a singer not to perform a Spanish version of the national anthem at a Dodgers game.

Latino fans — especially Mexican Americans — comprise a large percentage of the Dodgers' fan base, a trend that has been ongoing since the late 1980s, when Mexican-born left-handed pitcher Fernando Valenzuela played for the team.

Fun fact: The Dodgers are credited with helping spark the civil rights movement by calling up Jackie Robinson in 1947, which broke MLB's modern-day color line.

His courage paved the way for Black athletes across all sports as he endured racist taunts from opposing white managers and fans and had to travel amid segregation.

Robinson was friends with Martin Luther King Jr. and spent his post-playing career as a civil rights activist.

House Democrats and Republicans on Wednesday powered through flight cancellations and medical challenges in their efforts to return to Capitol Hill to vote on President Trump's "big, beautiful bill."

Why it matters: With the House divided by just a handful of votes, both parties are straining to ensure that as many of their members as possible are in attendance.

Republicans are furiously trying to stem defections on their side, with several groups of lawmakers unhappy with the Senate version of the bill meeting with Trump at the White House.

Democrats are using procedural tactics to delay the vote as long as possible and hoping their unanimous opposition to the bill leaves Republicans short of the votes they need to pass it.

Driving the news: Severe weather in D.C. on Tuesday caused members from across the country to face unexpected flight delays and cancellations, with some even stuck at layovers.

Several lawmakers, including Reps. Raja Krishnamoorthi (D-Ill.), Nancy Mace (R-S.C.) and Chris Deluzio (D-Pa.), opted to drive to D.C. rather than attempt to re-book their flights.

By Wednesday morning, Democrats were mostly present and voting while Republicans had to keep a procedural vote open for over an hour as their members straggled in.

Zoom in: Some Democrats were so determined to vote that they ventured to Capitol Hill just a day after surgery.

Rep. Joyce Beatty (D-Ohio), still in a wheelchair from a recent procedure, showed up with a cast over her eye, telling reporters she underwent eye surgery that she had scheduled for this week, thinking there wouldn't be votes.

Similarly, Rep. Jonathan Jackson (D-Ill.) had his arm in a sling, telling Axios he had planned rotator cuff surgery: "4th of July, how about that? I trusted them."

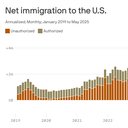

Data: Oxford Economics/Cato Institute/Deportation Data Project/CBO/DHS/TRAC. Chart: Axios Visuals

President Trump's immigration crackdown is hitting key pockets of the economy, disrupting workplaces and communities around the country.

Why it matters: The sharp fall in immigration this yearthreatens to slow down economic growth, particularly in the sectors and cities that relied on newcomers to the U.S. in recent years.

What they're saying: With the push against immigration, "the economy will find itself slightly diminished in the long run and inflation will run a touch higher," economist Bernard Yaros writes in a report for Oxford Economics.

There will be fewer workers to produce goods and services, slowing down growth and putting pressure on wages.

By the numbers: Net immigration started to fall last summer after the Biden administration took a harder line. This year, Trump's crackdown has been far more aggressive.

Net immigration — inflows of people minus outflows — is running at an annualized rate of 600,000, down about a third from where it was in the last three months of 2024, per the analysis by Oxford Economics, which looks at several sources of public data.

The decline is almost entirely due to a sharp drop in unauthorized immigration. Border crossings are stalled, and deportations are up.

What to watch: Yaros estimates in the long run, GDP will be 0.25% lower as a result.

That's a relatively modest macroeconomic effect, but there's a wild card. The "big, beautiful bill" that passed the Senate contains about $175 billion for even more immigration enforcement.

That could mean an even bigger decline going forward.

Between the lines: Immigration's effects on the economy are a slow burn, and it'll take a while before it shows up in the macro data.

For now they are rippling through industries that rely on immigrant workers, like farms, hotels, construction and meatpacking plants.

Zoom in: Smaller cities are feeling the hit from deportations and ICE raids, places like St. Louis, Buffalo and Pittsburgh where immigration had boosted faltering economies, the Wall Street Journal reports.

"The arrests cast a shadow over the local economy. Restaurant tables emptied. Kitchen workers stayed home. Fruit vendors disappeared from the streets. The number of shoppers at stores shrank, and those who still went didn't linger for long," the paper writes.

The nation's farms are in a tough spot, too, and employees are fearful of showing up to work.

"That means crops are not being picked and fruit and vegetables are rotting at peak harvest time," farmers and farmworkers told Reuters.

ICE is also going through carwashes, construction sites and meatpacking plants, the Washington Post reports.

In Los Angeles, immigration raids are slowing down the rebuilding efforts from the devastating fires earlier this year, the Los Angeles Times reports.

Even the horse racing industry is sweating the crackdown. "Scary times," a Louisville racehorse trainer tells a local news station about ICE raids.

Yes, but: Immigration opponents say the crackdown will translate into more and better-paying jobs for native-born Americans.

The bottom line: Until recently, a surge in immigration drove solid economic growth and a robust labor market. Now, policy is pushing it the other way.

If you're in the defense business, you've seen this meme in one form or another.

"Born too late to deploy to the Middle East," it reads.

"Born too early to deploy to the Middle East," it continues.

"Born just in time to deploy to the Middle East," it concludes.

Why it matters: Flippant? Yes. Compelling? Also yes, as the image's virality today reflects just how entangled the U.S. is in the troubled region, even as it promises to pivot more fully to the Chinese and Russian threat.

This is geopolitical tug of war, spiked with public cynicism.

Driving the news: Surprise strikes on Iranian nuclear facilities using B-2 Spirit bombers and 100-plus other aircraft marked Washington's latest foray into the Middle East, where for decades it's expended taxpayer dollars and lives. (Think Afghanistan, Iraq, Jordan, Kuwait, Lebanon, Syria and Yemen.)

Meanwhile, the Pentagon frets over Beijing and Moscow and their global ambitions. But the resources needed for that competition — including heavy-duty, traditional military hardware like aircraft carriers — are in high demand elsewhere.

Friction point: "There is a disconnect between what we, the United States, say in our national defense strategies and those sorts of products and what actually happens on the ground," Brian Carter, a Middle East expert at the American Enterprise Institute, told Axios.

"The problem is: We episodically prioritize the Middle East over China," he said. "Wehaven't been good about ensuring that we put enough effort into the Middle East to make sure that things don't spiral out of control."

"When we have to surge all this stuff in, we're always reactive."

Between the lines: Pentagon officials and military leaders have been hinting at this dynamic.

Elbridge Colby, the undersecretary of defense for policy, has long lobbied for prioritizing China over Europe and the Middle East. During his March confirmation hearing, Colby told senators the U.S. lacks "a multi-war military."

Indo-Pacific Command boss Adm. Samuel Paparo in November said support provided to Israel and Ukraine was "eating into" some of the most precious U.S. weapons stockpiles. In April, he revealed it took at least 73 flights to move a Patriot air-defense battalion out of China's backyard and into Central Command.

And most recently — just days ago — Acting Chief of Naval Operations Adm. James Kilby told lawmakers the Navy is chewing through Standard Missile-3s at "an alarming rate." The service has used more than $1 billion in munitions fighting Houthi rebels near the Red Sea and Gulf of Aden, and the USS Harry S. Truman has lost three Super Hornet aircraft, including one to friendly fire.

Zoom out: "The Middle East is the space where four things come together," Daryl Press, the faculty director at the Davidson Institute for Global Security, said in an interview.

The cities of Baltimore, Chicago and Columbus, Ohio, on Tuesday asked a federal court to overturn new regulations from Health Secretary Robert F. Kennedy Jr. that place tighter restrictions on Affordable Care Act enrollment.

Why it matters: Shortening the enrollment period and other changes would increase the uninsured and underinsured population and place more financial pressure on city-funded public health programs, the cities argue in their complaint.

They also argue that the loss of health insurance will make city residents less able to participate in civic lifeand have "cascading negative effects on city programs and communities."

The Main Street Alliance — a small business advocacy group — and Doctors for America are also plaintiffs in the lawsuit, which was filed in the U.S. District Court for Maryland.

State of play: Health and Human Services' regulation shortens the enrollment window for ACA plans on the federal insurance exchange and imposes a $5 monthly premium for consumers with fully subsidized coverage who are automatically reenrolled in ACA coverage, among other changes.

HHS projects the policies will decrease ACA exchange plan enrollment by between 725,000 and 1.8 million people.

The finalized rule "sets forth a wide range of changes that will render coverage on the Exchanges less affordable, less generous, and harder to obtain," the complaint reads.

The complaint states that the Trump administration violated administrative law in finalizing the rule.

But HHS maintains that its rule strengthens access to health insurance.

"The rule closes loopholes, strengthens oversight, and ensures taxpayer subsidies go to those who are truly eligible — that's not controversial, it's common sense," HHS communications director Andrew Nixon said in an email.

The agency has said the rule is necessary to improve program integrity in ACA markets and that it should lower enrollee premiums by 5% next year.

Majority Leader John Thune pressed Senate Republicans over the last 48 hours to go big or go home on the "big, beautiful bill." But over the next 24 hours, he'll learn if he broke the House's spirit in the process.

Why it matters: The Senate's spending cuts are deeper, the tax cuts are longer and the debt ceiling is steeper.

Thune (R-S.D.) lost three of his own members on his way to a 51-50 win, and he has left House Speaker Mike Johnson (R-La.) with a "non-starter," Rep. Ralph Norman (R-S.C.) told reporters.

One GOP lawmaker told Axios' Andrew Solender that Johnson is short "well over 20" votes.

Driving the news: It was an aggressive and risky move for a new majority leader, and it wasn't the light touch House leaders wanted.

But failure is a real possibility on Wednesday, with Johnson pronouncing himself "not happy with what the Senate did to our product."

Zoom out: All reconciliation bills eventually turn into a power struggle between the House and Senate.

In the first inter-chamber conflict of 2025, Thune actually lost the procedural battle. President Trump sided with the House and decreed that there would be one bill and not two separate ones.

But if the current Senate bill prevails, Thune will end up winning on three much more consequential issues: baseline policy, permanence for the business tax cuts, and the scope of entitlement reform.

Zoom in: For months, Thune and Senate Finance Chair Mike Crapo (R-Idaho) insisted that the Senate parliamentarian should use baseline policy to determine how much tax proposals will cost. This will have implications for future Congresses.

That accounting change, which gives Congress a pass on counting the cost of extending tax cuts that are on the books, allowed Crapo to make Trump's business tax cuts permanent, which was one of his top priorities.

Senate Republicans are convinced that will spur the kind of investment the economy will need to achieve 3% growth.

In all, the tax and spending cuts in the Senate amount to $3.3 trillion in deficit spending, compared to $2.8 trillion in the House, according to the Congressional Budget Office.

Between the lines: On the trickiest part of the Senate debate, lowering the threshold for the Medicaid provider tax, Thune maintained an aggressive and ideological posture.

"This is the first time we've done anything meaningful on entitlement reform," he told reporters.

With Sen. Rand Paul (R-Ky.) demanding a smaller debt ceiling increase, Thune was forced to negotiate with his old friend Sen. Lisa Murkowski (R-Alaska) for the 50th vote. Vice President Vance got him to 51.

Murkowski extracted changes to allow Alaska to keep more SNAP benefits and helped secure a $50 billion fund for rural hospitals.

The bottom line: Democrats are outraged by the cuts to the social safety net.

But the cuts were important enough to Thune and Senate conservatives to lose Sen. Thom Tillis (R-N.C.), who announced his retirement last weekend, and Sen. Susan Collins (R-Maine), the only GOP senator representing a state Kamala Harris won.

OCHOPEE, Fla. —President Trump began Tuesday by stoking his on-again feud with Elon Musk and joking about alligators chasing immigrant detainees.

He later basked in the Senate's passage of his signature tax and spending bill — and enthusiastically lobbed threats toward an array of perceived enemies, from immigrants to the media to Zohran Mamdani, New York City's Democratic nominee for mayor.

Why it matters: Trump and his team seemed to view it as his best day as president — a day when his brash, norm-crushing style was paying off in a series of "wins" in D.C. and Florida, where he visited a new immigration lockup dubbed "Alligator Alcatraz."

Reality check: To Trump's critics, it all seemed to capture what they see as his cruel recklessness.

Some warned that caging thousands of immigration detainees in tents on an airstrip in Florida's Everglades — during summer and hurricane season — was inviting an environmental and humanitarian disaster.

Trump brushed it off, and state officials pointed out the tents are air-conditioned.

Others noted that congressional analysts estimate 11.8 million Medicaid recipients could lose coverage under his big bill, which the analysts project would add $3.3 trillion to the nation's debt. And core inflation is rising, despite Trump's claims to the contrary.

"Could this not work out the way we want it to? Yes," a top Trump adviser said of the bill, which already is drawing fire from conservatives in the House who want debt reduction.

"If it doesn't work, then we have a problem," the adviser said. "And we'll deal with it. No other administration is better equipped to handle crisis."

Zoom out: Trump's White House began the week buoyed by a series of recent events.

On Saturday, his political committees announced a historic $1.4 billion war chest for the 2026 primaries.

The day before, the Supreme Court limited lower courts from using nationwide injunctions to block presidential policies nationwide.

And the weekend before that, Trump had ordered what the administration says were successful strikes on Iran's nuclear facilities.

Meanwhile, the stock market has regained the losses suffered after Trump's announcement of tariffs, which have added an additional $100 billion to U.S. coffers.

Trump's chipper vibe was evident early Tuesday, when he stopped to chat with reporters before boarding Marine One.

Wearing a red, "Gulf of America" cap, Trump threatened to sic DOGE on Musk after the billionaire criticized Trump's megabill.

"I don't think he should be playing that game," Trump said of Musk, warning that the DOGE "monster" could "eat Elon" by eliminating government subsidies to Musk's companies.

That was the first of what would be seven sessions Trump had with reporters on Tuesday. In subsequent ones, he:

Threatened to arrest Mamdani if the New York City Democrat is elected mayor and doesn't allow federal immigration officials to arrest undocumented immigrants in the city. Trump also called him a communist. (Mamdani said he wouldn't "accept this intimidation.")

Threatened to deport U.S. citizens who commit violent crimes, which isn't legal.

Threatened, along with Homeland Security Secretary Kristi Noem, to prosecute CNN for reporting about an app that warns people of immigration raids.

Also said CNN should face criminal charges for revealing an initial Pentagon estimate that said the strikes on Iran weren't as successful as Trump claimed. (CNN rejected the notion it did anything improper, noting the app is available to the public and that its report on the bombing assessment emphasized it was preliminary.)

The intrigue: Trump was magnanimous toward Florida Gov. Ron DeSantis, a close ally whom Trump dubbed "DeSanctimonious" when DeSantis challenged him in the 2024 GOP primaries. On Tuesday, Trump called him a friend.

"We have blood that seems to match pretty well," Trump said at the "Alligator Alcatraz" press conference.

Trump introduced DeSantis to Real America's Voice chief White House reporter Brian Glenn, noting the reporter is the boyfriend of Rep. Marjorie Taylor Greene (R-Ga.), a Trump loyalist who has expressed concern about the president's big bill.

"You think it's easy being with Marjorie?" Trump deadpanned to DeSantis.

Trump also described his relationship with DeSantis as a 10. Then he joked, "Maybe 9.9, because there might be a couple of little wounds."

When DeSantis asked Trump to remove a bureaucratic hurdle with the Army Corps of Engineers for an Everglades restoration project, Trump quickly granted it.

"Oh, I would do that. Let me ask myself permission," Trump said, pausing for a moment. "Permission granted! Go ahead and get the thing, get it complete."

Later in the day, the White House said the University of Pennsylvania, under pressure from Trump's administration, had retroactively stripped the records and titles of transgender swimmer Lia Thomas.

Thomas' participation in the NCAA women's swim championships in 2022 helped inspire Trump's push against transgender women in women's sports.

Trump then wrapped up the day by announcingIsrael had agreed to a ceasefire with Hamas in Gaza. Trump urged Hamas to accept the deal.

"Look at the press I'm getting!" Trump crowed to his team at one point, as he kept returning to the cameras and reporters.

Editor's note: This story has been updated to state that the tariffs have added $100 billion to U.S. coffers (not $100 million).